Effective January 15, 2022, group health plans and health insurers must cover over-the-counter (OTC) COVID-19 tests without any cost-sharing requirements, prior authorization or other medical management requirements. However, carriers have implemented a range of solutions with each one doing it slightly differently. This presents a communication challenge for employers when guiding participants through their OTC COVID-19 test coverage.

The guidance significantly expands access to free and low-cost COVID-19 at-home tests. Insurers must cover up to eight FDA-authorized rapid tests per member per month, including dependents, but the guidance doesn’t dictate how insurers manage this coverage process. This results in the spectrum of approaches we’ve seen from carriers, rather than one universal process, and an abundance of client questions.

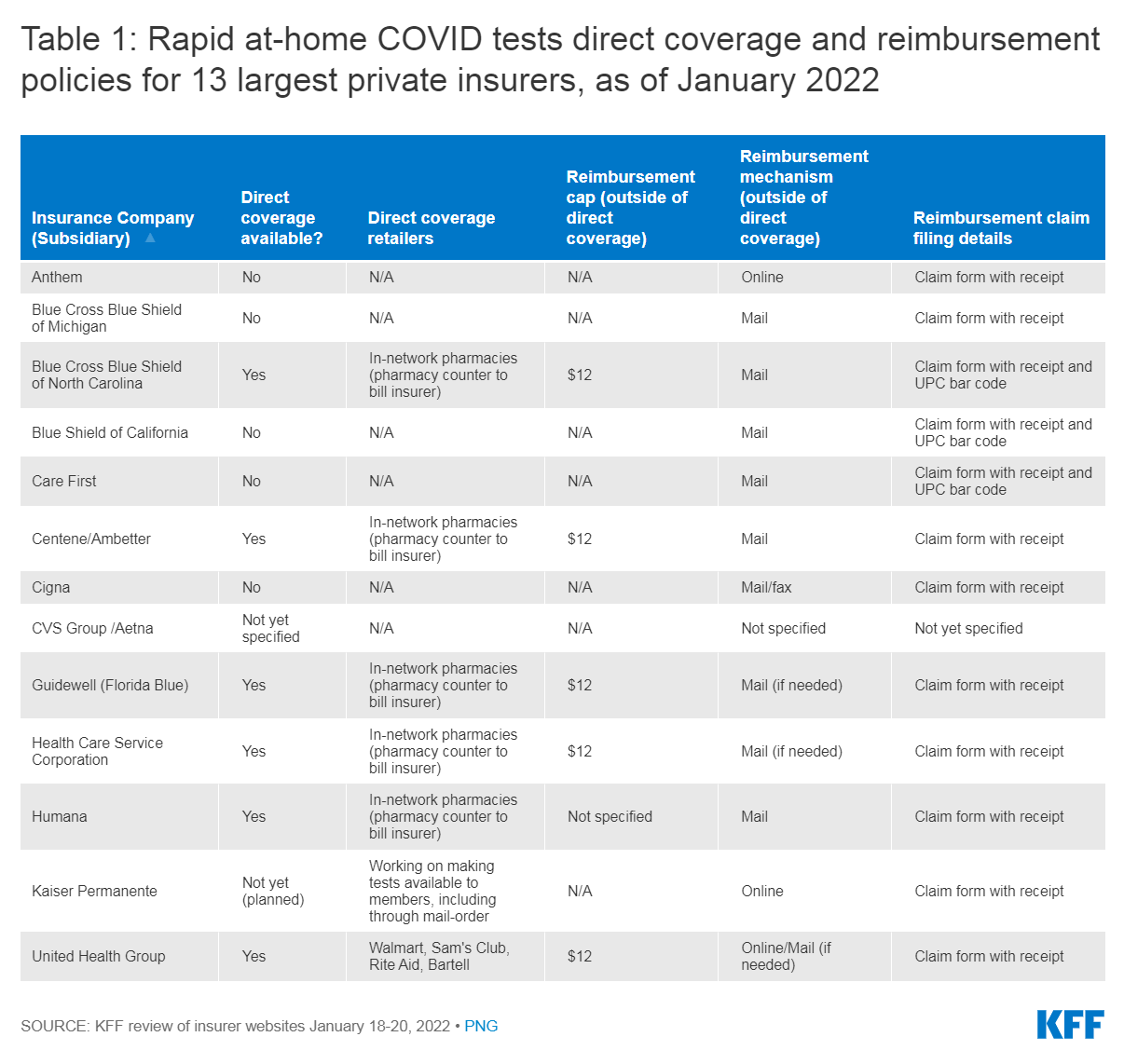

Research by KFF details the split among major insurers between “direct coverage” and “reimbursement” options with varying details for individual coverage processes. Seven of the 13 largest insurers are currently using various reimbursement policies, and six have direct coverage options. This may also be handled through a third-party administrator or pharmacy benefit manager.

As KFF’s chart shows, each process is slightly different and both direct coverage and reimbursement options come with nuances.

For reimbursement, submission processes vary between mail and online submission and what forms and information are required. The upfront costs necessary before reimbursement can also present obstacles for low-income participants.

For direct coverage, members must purchase tests through certain retailers, pharmacies, or direct-to-consumer programs, again depending on carrier. If these members purchase tests outside of participating retailers, they can also apply for reimbursement. This is capped at $12 and the process varies by carrier.

Employee education and HDHPs can promote cost-conscious behavior.

Clear communication is especially important if the employer offers plans from multiple carriers.

Additionally, these covered tests cannot be used to fulfill any employer-mandated testing requirement. Some carriers are requiring members to provide attestations that the covered test will not be used for employment purposes. This messaging must also be clearly provided to employees.

Plans and insurers can place other limits on coverage including setting limits on the number or frequency of tests that are covered (as long as the insurer provides at least eight tests per month without cost-sharing) and taking steps to prevent, detect and address fraud and abuse.

Employers and plan sponsors should connect with their insurance carrier or third-party administrator to understand how this new requirement will impact their plans, including which pharmacies or retailers will be making the tests available in-network. Then, they should ensure that they communicate this new coverage requirement to employees and plan participants.

Our experts discuss navigating OTC COVID-19 test coverage and more in the Compliance Briefing below:

For additional information on OTC COVID-19 test coverage, please see the January 11 Compliance Alert on the Compliance Resource Page.